Originally posted on medvisory.ca

listen to the blog in audio format!

Most Canadians think of RRSP or TFSA accounts as vehicles for holding mutual funds, exchange-traded funds, or publicly listed stocks. What many do not realize is that these registered accounts can also be used to invest in real estate, specifically through private mortgages, offering the potential for substantially higher returns than traditional investment vehicles while still benefiting from the same tax advantages these accounts provide.

For physicians and other high-income professionals looking to diversify their wealth-building strategy, understanding how to use a RRSP or TFSA for mortgage-based real estate investing is a valuable piece of financial knowledge that is often overlooked.

What Most People Get Wrong About RRSP or TFSA Investing

The common assumption is that RRSP or TFSA accounts are limited to publicly traded securities, but this is a misconception that prevents many Canadians from taking full advantage of their registered savings. Under Canadian tax rules, mortgages are recognized as qualified investments that can be held within a self-directed RRSP or TFSA account, meaning you can effectively become a private mortgage lender and collect interest payments on those loans, all within a tax-sheltered or tax-free structure.

This matters because private mortgage lending can generate annual returns in the range of eight to twelve percent, a figure that significantly outpaces the average returns on many conventional registered account investments. For a physician who is already maximizing contributions to their RRSP or TFSA and looking for ways to improve the performance of those funds, this approach offers a compelling alternative worth serious consideration.

It is important to distinguish this from investing in publicly listed real estate investment trusts or real estate company stocks through a registered account. While those are also valid strategies, investing in private mortgages through a self-directed RRSP or TFSA provides a more direct connection to the underlying real estate asset and typically offers stronger returns, though with a different risk profile.

How to Use Your RRSP or TFSA to Fund Private Mortgages

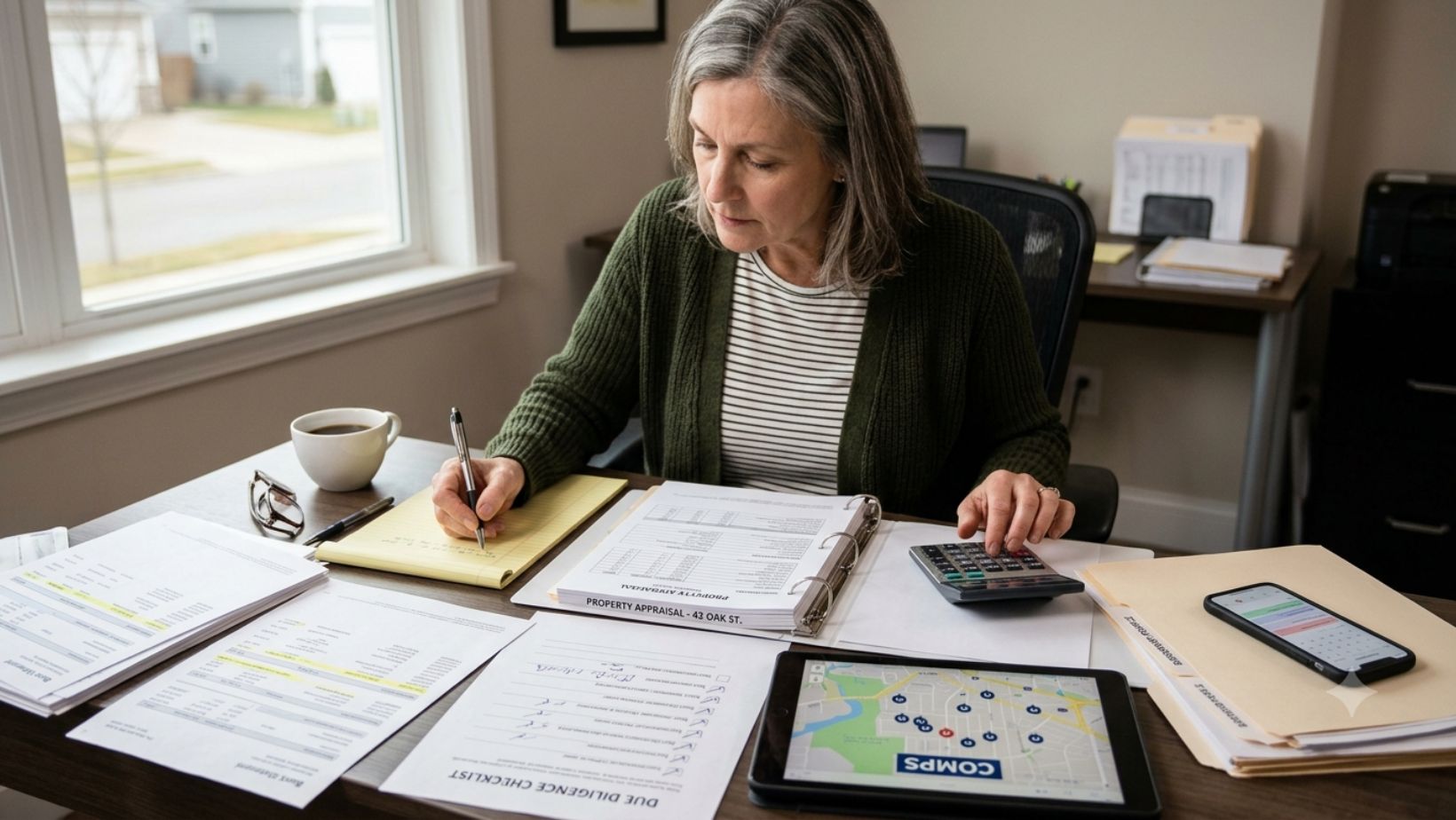

The process of investing through a self-directed RRSP or TFSA in private mortgages involves several steps, each of which requires careful attention to ensure the investment is set up correctly and legally protected. The first step is finding a trustee institution that allows mortgage investments within a self-directed registered account. Not all financial institutions offer this option. In Canada, institutions such as Olympia Trust and Community Trust are examples of trustee companies that facilitate this type of arrangement. To get started, you would need to open a self-directed RRSP or TFSA account with one of these institutions, or transfer existing registered funds into a self-directed account. This process generally involves completing paperwork to establish the account and designate the amount you wish to deploy toward mortgage lending. Once your self-directed account is set up, the next step is identifying a suitable borrower. Many borrowers who seek private mortgage financing do so because the strict lending criteria applied by major chartered banks limit their ability to qualify for conventional financing, even when the underlying property and their financial position are sound. These borrowers are typically willing to pay higher interest rates in exchange for access to private capital, which is what makes this arrangement attractive for lenders. One practical way to connect with borrowers and mortgage professionals who facilitate these arrangements is through real estate investment seminars and networking events. Mortgage brokers who specialize in alternative lending are another valuable contact, as they regularly work with borrowers who need private financing and can connect you with suitable opportunities.What Due Diligence Looks Like Before Lending

Before committing any funds from your RRSP or TFSA to a private mortgage, conducting thorough due diligence is essential. This is not a passive investment in the same way that purchasing an index fund is passive. You are making a direct lending decision, which means the quality of that decision depends on the quality of the information you gather and analyze beforehand.

Start by reviewing the borrower’s financial history, including their credit report, income documentation, and any existing debt obligations. A borrower’s credit profile gives you a sense of their repayment reliability and overall financial management. You should also obtain a property appraisal completed by an accredited appraiser to confirm that the property’s market value supports the loan amount you are being asked to provide.

Beyond the borrower and the property itself, studying the broader market conditions in the area where the property is located is equally important. This includes reviewing recent sale prices, days on market for comparable properties, vacancy rates, and general demand trends. Tools such as HouseSigma, a Canadian real estate data platform, can help you research local market conditions and comparable sales to assess whether the underlying economics of the market are strong enough to support your investment.

The loan-to-value ratio, which compares the loan amount to the appraised value of the property, is one of the most important figures to evaluate. A lower loan-to-value ratio means there is more equity in the property relative to the loan, which provides a greater buffer for recovering your capital if the borrower defaults and the property needs to be sold.

A lawyer must also be involved in closing the transaction. The borrower typically covers the legal costs, and the lawyer plays a critical role in ensuring your interest is protected by registering a legally enforceable charge against the property title on your behalf. This registration is what gives you a formal, legally recognized claim on the property in the event of a default.